What Happens to Personal Debts When You register an llp Entity?

Curious about how your personal finances are affected when you register an llp? Get expert insights from CA4Filings on liability protection and debt.

Many entrepreneurs starting their business journey often worry about the safety of their personal assets. If you are planning to register an llp, one of the primary questions we frequently address at CA4Filings is how this decision impacts your existing or future personal debts. Deciding to formalize your venture through Company Registration is a significant step, and understanding the legal boundary between your personal finances and your business is crucial for peace of mind.

When you register an llp, you are essentially creating a distinct legal persona for your business. This separation is the cornerstone of modern business structure, but it is often misunderstood. Let’s break down how this works in the Indian context and what it means for your wallet.

The Concept of Limited Liability: A Protective Firewall

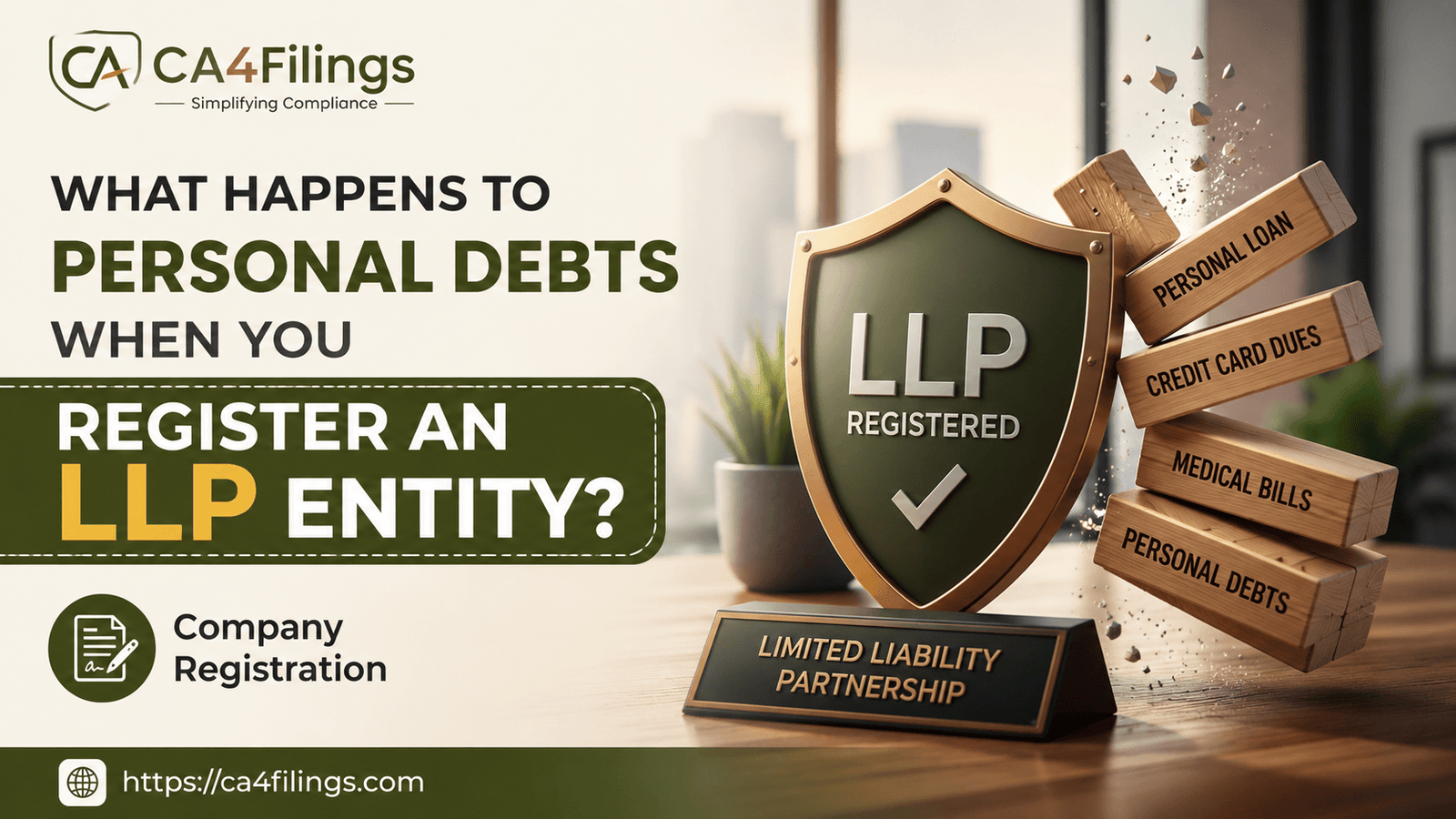

The most significant advantage when you register an llp (Limited Liability Partnership) is the concept of limited liability. In a traditional sole proprietorship or a general partnership, there is no legal distinction between the owner and the business. If the business defaults on a loan, your personal car, savings, and even your home could theoretically be at risk.

However, an LLP acts as a commercial liabilities firewall. Because the entity is a separate legal body, the debts incurred by the business belong to the entity itself, not the partners personally. This provides a level of individual protection limits that sole traders simply do not enjoy.

Does Personal Debt Automatically Become Business Debt?

A common misconception we see is the idea that transferring personal debts into the LLP is a simple way to "clean" one's balance sheet. To be clear: when you register an llp, your existing personal debts do not automatically move over to the business.

Existing Debts: If you took a personal loan to fund your initial setup before incorporating, that debt remains strictly yours.

New Business Debts: Any new loans taken in the name of the LLP are the responsibility of the LLP. If the LLP runs out of funds, creditors generally cannot chase you for your personal assets, provided there was no fraud or personal guarantee involved.

Personal Bankruptcy Separation and the Role of Personal Guarantees

While the law creates a buffer, it is not an absolute shield. In India, most banks are well-aware of the personal bankruptcy separation offered by an LLP structure. Consequently, when a startup or SME approaches a bank for a business loan, lenders almost always insist on a "Personal Guarantee."

Why Personal Guarantees Matter

Even after you register an llp, banks will often require the designated partners to sign a personal guarantee. By doing so, you are voluntarily stepping outside the protective bubble of the LLP. If the business fails to pay the loan, the bank has the right to go after your personal assets, effectively bypassing the limited liability protection.

When you sit down to register an llp, always consider your creditworthiness. Lenders evaluate your credit scoring parameters alongside the business's projected revenue. If your personal credit score is low, even an LLP structure might struggle to secure debt without a high-value collateral or personal guarantee.

How to Manage Debts Effectively After Registration

Once you decide to register an llp, follow these professional tips to ensure your personal and business finances remain distinct:

Maintain Separate Bank Accounts: Never mix business revenue with personal expenses. This is the first step toward maintaining a clean "corporate veil."

Formalize Capital Contribution: Document every rupee you inject into the business as capital. This clarifies that you are a creditor of the business, not just the owner.

Audit Your Guarantees: Be extremely cautious about signing personal guarantees. Try to build the business’s credit history early so that future loans can be secured on the LLP’s own merit.

Professional Bookkeeping: Proper financial reporting proves that the LLP is a functional, independent entity, which strengthens your legal standing should a creditor ever challenge the separation.

Frequently Asked Questions

1. Does my CIBIL score affect the LLP’s ability to get a loan?

Yes, especially in the early stages. While you register an llp to separate liability, lenders still look at the partners' personal credit history to gauge the reliability of the management.

2. Can creditors seize my personal house if the LLP goes bankrupt?

Generally, no, unless you have signed a personal guarantee for the LLP's debts. This is the primary reason why business owners register an llp—to protect personal property.

3. If I register an llp, are my partners responsible for my personal debts?

No. Your personal debts remain your own. Your partners have no liability toward your individual financial obligations, and vice-versa.

4. Is the cost to register an llp worth the debt protection?

Absolutely. The long-term protection against business-related financial losses far outweighs the initial registration and compliance costs.

Choosing to register an llp is a strategic move that brings professionalism and, more importantly, a vital layer of security to your entrepreneurial journey. While it isn't a "get out of jail free" card for your personal debts, it establishes a formal boundary that protects your personal future from business-related risks.

If you are ready to take the next step and register an llp, do not go at it alone. At CA4Filings, we specialize in simplifying the complex regulatory landscape of India. Our experts are here to help you structure your business, manage your liabilities, and keep your finances secure. Contact CA4Filings today, and let’s get your business started on the right legal footing!

Latest Updates

ca4filings.com Services

-registration.png)